How To Determine if You’re Ready To Buy a Home

If you’re trying to decide if you’re ready to buy a home, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates and home prices, the limited supply of homes for sale, and more. And, you’re juggling how all of those things will impact the choice you’ll make.

While housing market conditions are definitely a factor in your decision, your own personal situation and your finances matter too. As an article from NerdWallet says:

“Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.”

Instead of trying to time the market, focus on what you can control. Here are a few questions that can give you clarity on whether you’re ready to make your move.

1. Do You Have a Stable Job?

One thing to consider is how stable you feel your employment is. Buying a home is a big purchase, and you’re going to sign a home loan stating you’ll pay that loan back. That’s a big commitment. Knowing you have a reliable job and a steady stream of income coming in can help put your mind at ease when making such a large purchase.

2. Have You Figured Out What You Can Afford?

If you have reliable paychecks coming in, the next thing to figure out is what you can afford. That’ll depend on your spending habits, debt, and more. To be sure you have a good idea of what to expect from a number’s perspective, start by talking to a trusted lender.

They’ll be able to tell you about the pre-approval process and what you’re qualified to borrow, current mortgage rates and your approximate monthly payment, closing costs to anticipate, and other expenses you’ll want to budget for. That way you can make an informed decision about whether you’re ready to buy.

3. Do You Have an Emergency Fund?

Another key factor is whether you’ll have enough cash left over in case of an emergency. While that’s not fun to think about, it’s an important thing to consider. You don’t want to overextend on the house, and then not be able to weather a storm if one comes along. As CNET says:

“You’ll want to have a financial cushion that can cover several months of living expenses, including mortgage payments, in case of unforeseen circumstances, such as job loss or medical emergencies.”

4. How Long Do You Plan To Live There?

It was mentioned above, but buying a home involves some upfront expenses. And while you’ll get that money back (and more) as you gain equity, that process takes time. If you plan to move too soon, you may not recoup your investment. For example, if you’re looking to sell and move again in a year, it might not make sense to buy right now. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Five years is a good, comfortable mark. If the price of your home appreciates considerably, then even three years would be fine.”

So, think about your future. If you plan to transfer to a new city with the upcoming promotion you’re working toward or you anticipate your loved ones will need you to move closer to take care of them, that’s something to factor in.

5. Above all else, the most important question to answer is: do you have a team of real estate professionals in place?

If not, finding a trusted local agent and a lender is a good first step. The pros can talk you through your options and help you decide if you’re ready to take the plunge or if you have a few more things to get in order first.

Bottom Line

If you want to have a conversation about all the things you need to consider to determine if you’re ready to buy, let’s connect.

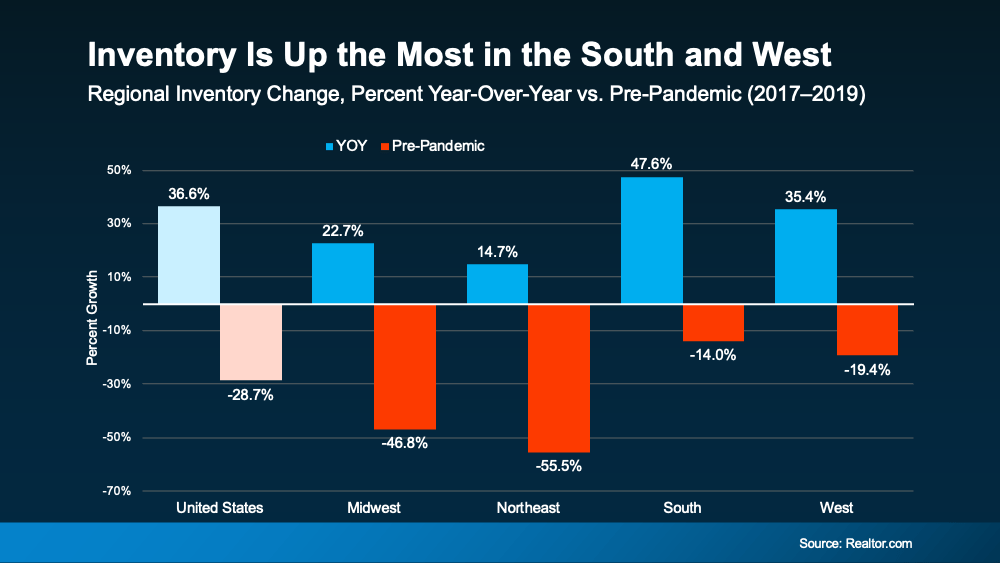

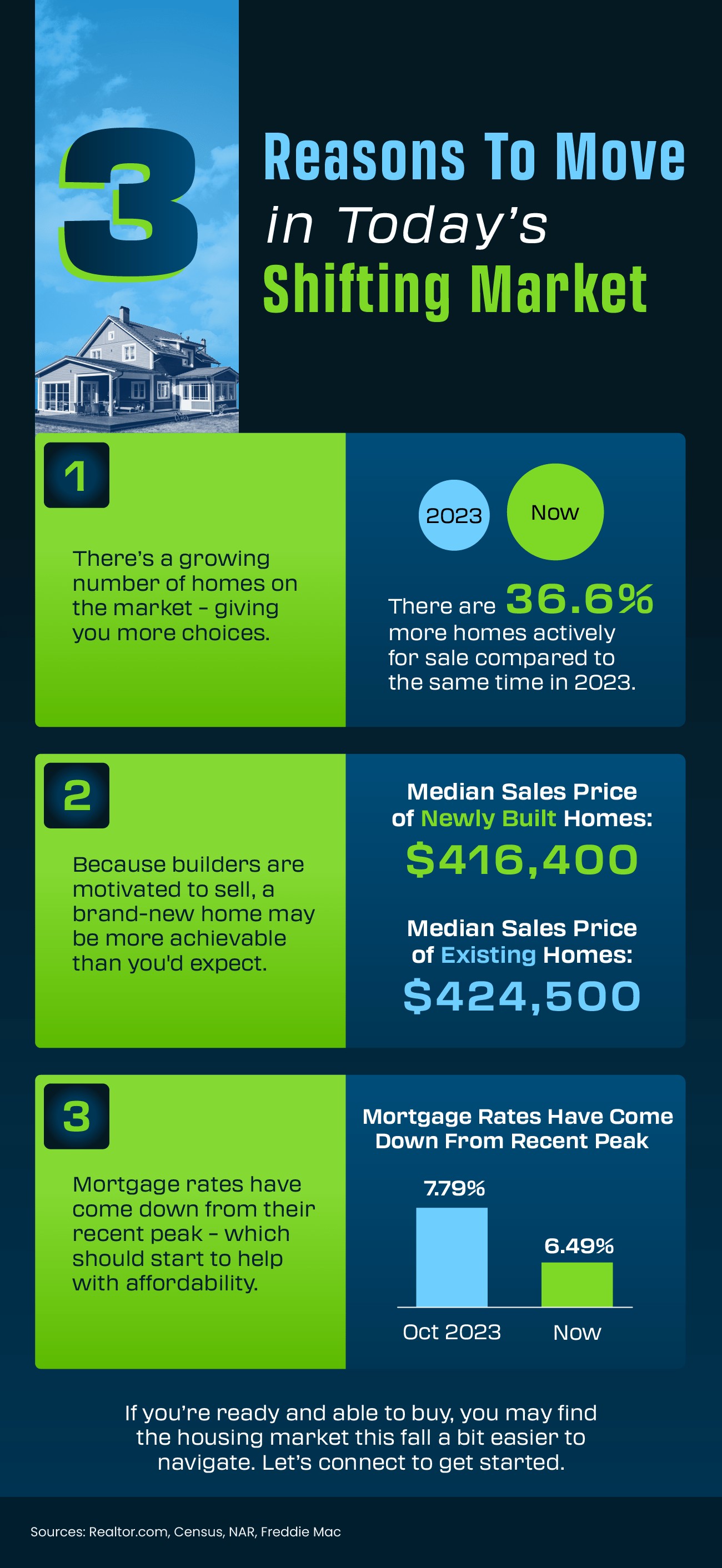

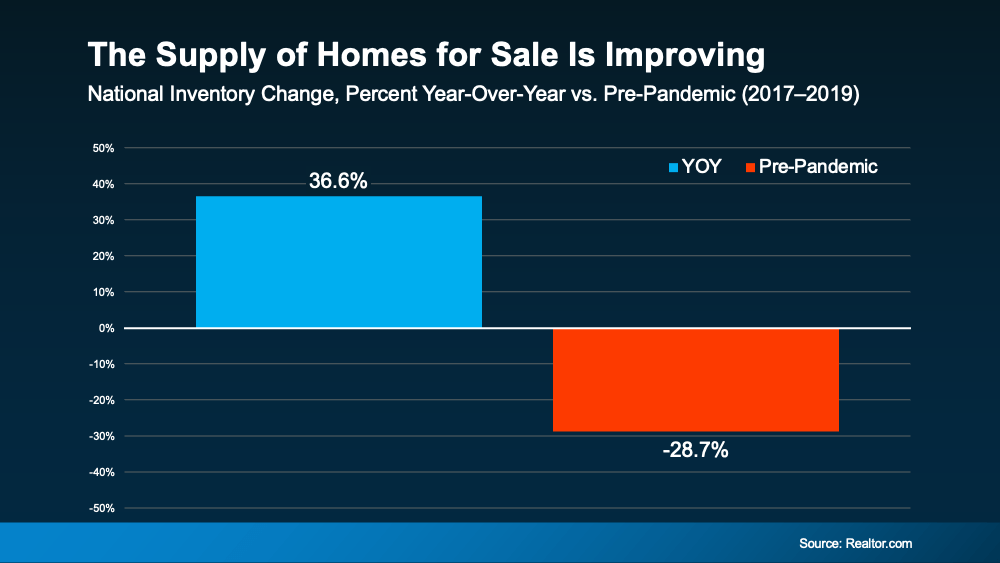

So, while we’re up by almost 37% year-over-year, we’re still not back to how much inventory there’d be in a normal market.

So, while we’re up by almost 37% year-over-year, we’re still not back to how much inventory there’d be in a normal market.