Outdoor Projects Can Boost Curb Appeal When You Sell [INFOGRAPHIC]

Some Highlights

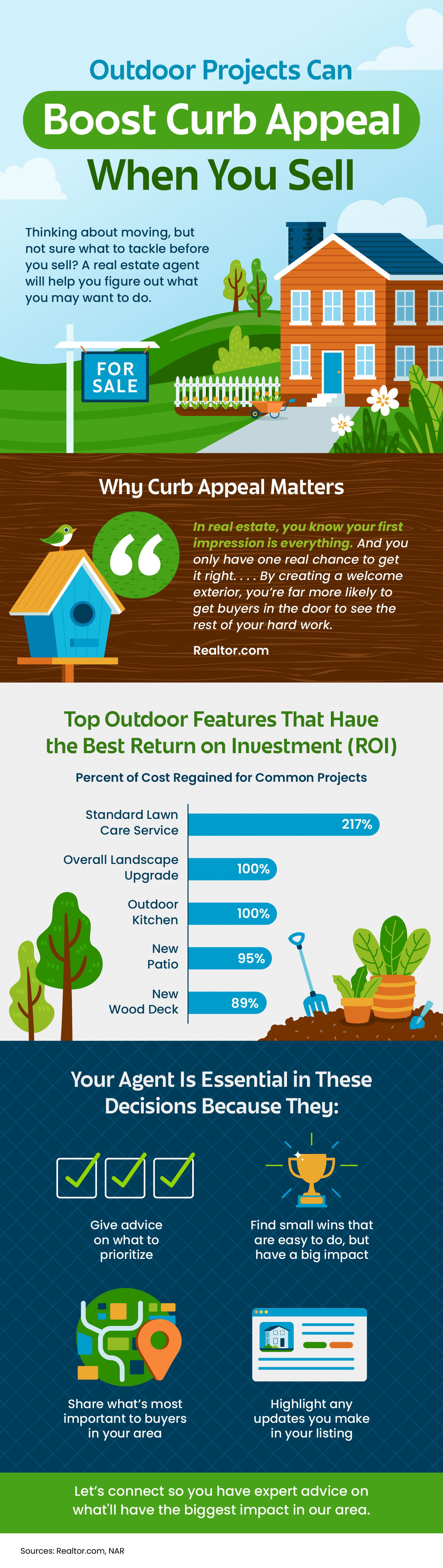

- In real estate, a good first impression is key. If the outside of a house looks welcoming, more people will want to come in and see it.

- Your agent helps you by giving advice on what you may want to prioritize, finding easy fixes that make a big difference, knowing what buyers in your area like, and showing off your updates in your listing.

- Let’s connect so you have expert advice on what’ll have the biggest impact in our area.